Table Of Content

Take some of your extra money and put it toward your mortgage principal every month to pay off the loan faster. Compare customized mortgage rates from Canada’s best lenders and brokers for free. It’s a lot more work than a mortgage pre-qualification, but pre-approval is a necessary step in the home buying process. Once you’re pre-approved, you’ll be able to bid confidently on a home that you know you can afford. With pre-approval, you’ll be asked to provide several documents, including banking and employment information, that your lender will then verify.

Three Homebuyers' Financial Situations

For a mortgage loan, the borrower often is also referred to as the mortgagor (and the bank or lender the mortgagee). If you wait, you may be able to get a better interest rate later, which could save you thousands of dollars in the long run. And buying a home means assuming the risk that the property’s value could fall, or that it might need expensive repairs sometime down the line. If you postpone a home purchase, you can put off those risks until you’re in a better financial position. The mortgage rate you’re offered has a big effect on whether you can afford a home.

Tips to Improve Your DTI Ratio

You can get a flood insurance quote from the National Flood Insurance Program, but private insurers may be able to offer a better deal. Let’s say your car payment, credit card payment and student loan payment add up to $1,050 per month. Your proposed housing payment, then, could be somewhere between 26% and 35% of your income, or $1,820 to $2,450. Generally, the higher the credit score you have, the lower the interest rate you’ll qualify for and improve overall what you can afford in a home. Even lowering your interest rate by half a percent can save you thousands of dollars and increase your affordability range significantly. Your other two options, pay off debt and increase income, take time.

Mortgage default insurance

As a homeowner, you’ll pay property tax either twice a year or as part of your monthly home payment. This tax is a percentage of a home’s assessed value and varies by area. For example, a $500,000 home in San Francisco, taxed at a rate of 1.159%, translates to a payment of $5,795 annually.It’s important to consider taxes when deciding how much house you can afford. When you buy a home, you will typically have to pay some property tax back to the seller, as part of closing costs.

Frequently asked questions about mortgage affordability

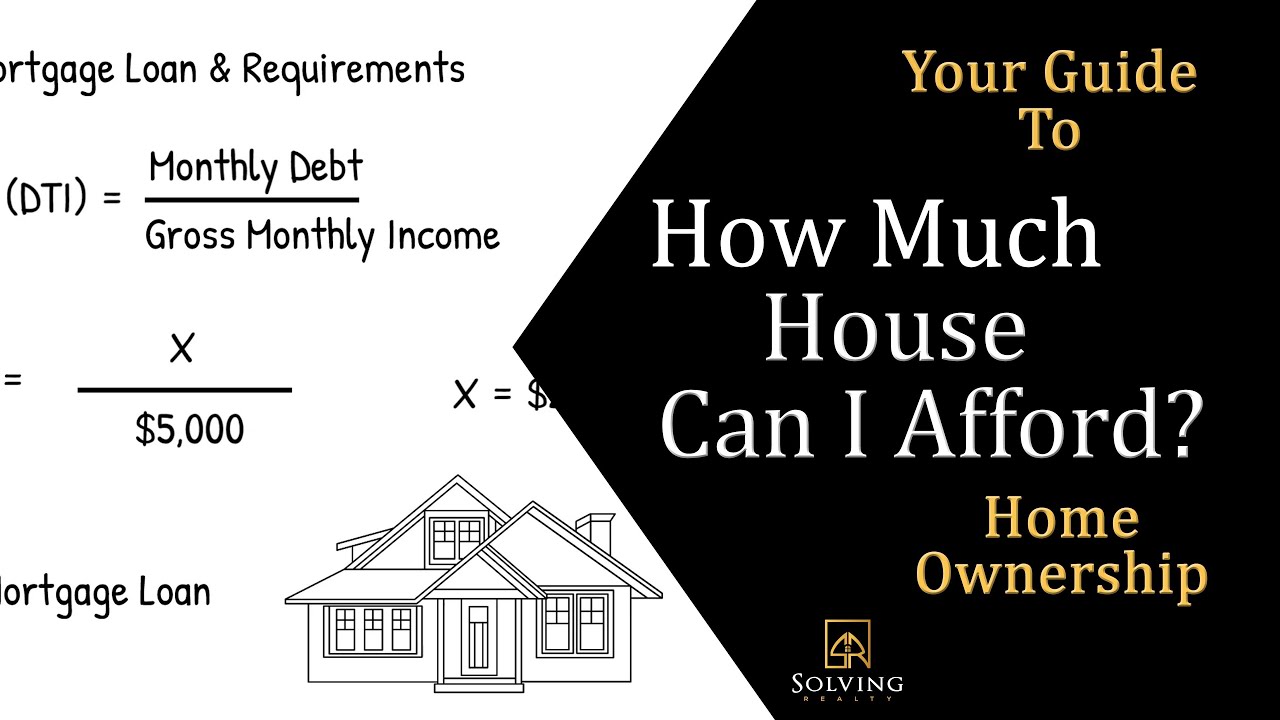

In addition to housing costs, your total monthly debt load would include credit card interest, car payments and other loan expenses. The sum of your total monthly debt load as a percentage of your gross household income is your TDS ratio. Your debt-to-income ratio is the percentage of pretax income that goes toward monthly debt payments, including the mortgage, car payments, student loans, minimum credit card payments and child support. Lenders look most favorably on debt-to-income ratios of 36% or less — or a maximum of $1,800 a month on an income of $5,000 a month before taxes.

Applying for a new mortgage or renewing your current loan with a new lender will require passing the mortgage stress test. If you want to increase how much you can borrow, thus increasing how much you can afford to spend on a home, there are few steps you can take. However, on July 5, 2021, these updated requirements for insured mortgages were reversed, and the GDS and TDS limits reverted to 39% and 44%, respectively. Following brisk sales in the first few months of the year, affordability declined further for home buyers in March, based on the latest Affordability Report compiled by Ratehub.ca.

Home insurance

Therefore, this compensation may impact how, where and in what order products appear within listing categories, except where prohibited by law for our mortgage, home equity and other home lending products. Other factors, such as our own proprietary website rules and whether a product is offered in your area or at your self-selected credit score range, can also impact how and where products appear on this site. While we strive to provide a wide range of offers, Bankrate does not include information about every financial or credit product or service. To calculate how much house you can afford, we’ve made the assumption that with at least a 20% down payment, you might be best served with a conventional loan.

How Much House Can I Afford On A $120K Salary? - Bankrate.com

How Much House Can I Afford On A $120K Salary?.

Posted: Tue, 03 Oct 2023 07:00:00 GMT [source]

Mortgage affordability refers to how much you’re able to borrow based on your current income, debt and living expenses. The higher your mortgage affordability, the more expensive a home you can afford to purchase. This month’s edition finds Toronto home buyers saw affordability decrease by the largest margin, as home prices there increased $19,700 to an average of $1,113,600. As a result, borrowers must have an income that’s $3,400 higher than last month to qualify for a mortgage on the average priced home in the city. USDA loans require no down payment, and there is no limit on the purchase price.

Home Affordability Calculator

You’ll also need to estimate your future home’s utility bills for electricity, gas, trash and water. You might not be paying for all of these expenses where you live now, or you might be paying less for them because you’re in a smaller place than your future home will be. To get an idea of the costs, ask people who already live in the area where you want to buy. Fees depend on how many amenities the community has, how many services it requires, and how much upkeep it needs. Local real estate listings can give you an idea about the homeowners association fees in the neighborhoods, condos or townhomes you’re interested in. Closing costs, which will run you about 2% to 5% of the purchase price, will affect how much home you can afford to a greater or lesser extent depending on how you pay for them.

In other words, the sum of monthly housing costs and all recurring secured and non-secured debts should not exceed 41% of gross monthly income. VA loans generally do not consider front-end ratios of applicants but require funding fees. FHA loans have more lax debt-to-income controls than conventional loans; they allow borrowers to have 3% more front-end debt and 7% more back-end debt. The reason that FHA loans can be offered to riskier clients is the required upfront payment of mortgage insurance premiums. If your down payment is less than 20 percent of your home's purchase price, you may need to pay for mortgage insurance. You can get private mortgage insurance if you have a conventional loan, not an FHA or USDA loan.

These are all solid choices, except for making only the minimum payments on your bills. Having less debt can improve your credit score and increase your monthly cash flow. In the U.S., conventional, FHA, and other mortgage lenders like to use two ratios, called the front-end and back-end ratios, to determine how much money they are willing to loan. They are basic debt-to-income ratios (DTI), albeit slightly different and explained below.

No comments:

Post a Comment